Boat loans commonly run from 5 to 20 years. Many secured marine loans offer 10-, 15- or 20-year terms for qualifying borrowers, while smaller unsecured loans may have shorter repayment periods. The maximum term depends on the loan amount, boat age and condition, lender policy, borrower credit profile, down payment and whether the loan is secured by the vessel. Used boats can also qualify for long-term financing, so there is no universal 10- or 12-year limit.

How Long Do Boat Loans Typically Last?

For many consumers planning to purchase a yacht or recreational boat, aside from the price of the vessel itself, the questions they are most concerned about are often: "How long do boat loans typically last?" "What is the most cost-effective loan term?" and "Are the loan terms the same for new and used boats?"

Used boats do not have a universal maximum loan term. Some lenders limit older vessels to shorter terms, while others may offer 15- or 20-year financing on qualifying used boats. The result depends on the vessel’s age, condition, valuation, loan amount, maintenance records and the lender’s underwriting policy.

| Loan Term Type | Typical Duration | Common Boat Types | Best For |

|---|---|---|---|

| Short-Term Boat Loan | 5–7 years | Small Powerboats, older used boats, lower-priced recreational boats | Lower total interest and faster payoff |

| Medium-Term Boat Loan | 8–12 years | Midsize boats, sailboats, family cruisers, motor yachts | Balanced monthly payments and manageable interest |

| Long-Term Boat Loan | 15–20 years | New luxury yachts, high-value motor yachts, large vessels | Lower monthly payments and improved cash flow |

In many yacht-purchasing scenarios, buyers typically opt for a 5–10-year loan, as this keeps total interest expenses relatively manageable; however, those planning long-term cruising or investing in charter operations may choose a loan term of 15 years or more to optimize cash flow.

Loan Term Policies of Different Lenders

Different banks and financial institutions have varying policies regarding boat loans:

- Commercial Banks: Low interest rates and relatively complex loan processes, but they typically offer longer terms, making them suitable for clients with ample funds.

- Specialized Yacht Lenders: Fast approval times and flexible loan solutions tailored to different boat models, but interest rates are slightly higher.

- Credit Unions/Small Financial Institutions: Suitable for loans on small to medium-sized boats, with flexible interest rates and terms, but loan amounts may be limited.

Secured vs Unsecured Boat Loan Terms

Boat loan terms vary depending on the financing type, loan amount, and intended use. The following table highlights the key differences between secured, unsecured, and commercial boat loans.

| Loan type | Common characteristics | Effect on term |

|---|---|---|

| Secured marine loan | Boat is used as collateral; usually available for higher loan amounts | May offer 10–20-year terms |

| Unsecured personal loan | No boat collateral; approval depends mainly on borrower credit and income | Usually shorter terms and smaller loan amounts |

| Commercial marine financing | Intended for charter or business use | Separate underwriting, documentation and insurance requirements |

Choosing the right loan type depends on your boat value, financial situation, and usage plan. Understanding these differences can help you select a suitable financing option.

How Old of a Boat Can You Finance?

There is no single maximum boat age accepted by every lender. Some lenders restrict older boats or shorten the available loan term, while specialist marine lenders may consider older vessels when the survey, valuation, maintenance history, insurance and borrower profile are satisfactory.

Buyers financing an older boat should expect the lender to request more documentation and should not assume that a 15- or 20-year term will be available solely because the purchase price is high.

Can You Get a 20-Year Boat Loan?

Yes. Some banks, credit unions, and specialist marine finance providers offer flexible loan terms for qualifying applications. According to BoatUS, boat loan terms can vary depending on factors such as the loan amount, vessel type, age, and borrower qualifications, with some marine loans offering repayment periods ranging from shorter terms to longer-term financing options. Availability depends on the lender’s underwriting standards, collateral value, credit profile, and financing policy. For example, marine lenders and credit unions in the U.S. market may publicly advertise extended repayment terms for eligible boat buyers. Buyers should always verify the current loan term, APR, fees, and prepayment conditions directly with the lender before applying.

Key Factors Affecting the Term of a Boat Loan

The term of a loan is not set arbitrarily but is determined by multiple factors. Understanding these factors can help boat buyers make more informed decisions when applying for a boat loan, ensuring manageable monthly payments while minimizing interest expenses. The following are the main factors that influence the term of a boat loan:

Boat Price and Loan Amount

The vessel’s price and the loan amount are typically among the most significant factors influencing the loan term. Generally, the higher the loan amount, the more likely banks are to offer longer repayment terms to reduce the borrower’s monthly payment burden. For high-end luxury yachts, if the loan term is too short, the monthly payments may exceed the budget of many buyers.

Down Payment Ratio

The higher the down payment ratio, the lower the risk for the lender, so they are generally more willing to offer longer loan terms and more competitive interest rates. For banks, a high down payment indicates that the borrower has stronger financial resources and repayment capacity. Generally, clients who make a down payment of 20%–30% are more likely to secure approval for long-term loans. In my experience, many clients who increase their down payment not only successfully extend their loan terms but also lower their overall financing costs. Therefore, if your budget allows, increasing the down payment is often a wise choice.

Vessel Age and Type

Vessel age and type are key factors banks consider when assessing a boat’s value. New boats generally have higher market value and better retention of value, making them more eligible for long-term loans. Conversely, older used boats, due to higher risks of future depreciation and maintenance costs, often result in shorter loan terms. Additionally, vessel types and brands with high market recognition are more favored by lenders. For example, internationally renowned brands such as Beneteau, Sea Ray, Princess, and Azimut, which have mature second-hand markets and strong value retention, typically qualify for longer loan terms.

Borrower’s Credit Score

Credit score is one of the key factors determining loan approval. For U.S. boat buyers, the higher the FICO credit score, the greater the chance of securing a long-term loan with a low interest rate. Generally, borrowers with a credit score of 720 or higher are more likely to obtain favorable loan terms. Conversely, if a borrower has a limited credit history or a low score, lenders may shorten the loan term or even require a higher down payment.

Lenders’ Risk Assessment Criteria

Different lenders assess risk in slightly different ways, so applying for a loan for the same boat at different institutions may result in varying loan terms and interest rates. In addition to the borrower’s financial situation, banks also consider factors such as the boat’s intended use, maintenance history, mooring location, and insurance coverage. For example, vessels used for personal leisure and recreation typically carry lower risk; conversely, vessels used for commercial charter or charter operations—due to their higher frequency of use—may result in lenders requiring a higher down payment, a shorter loan term, or additional collateral. When recommending loan options to clients, I typically match them with financial institutions based on the vessel’s actual use, thereby increasing the approval rate and securing more favorable loan terms.

How Should You Choose a Boat Loan Term?

Choose the shortest loan term whose monthly payment remains affordable after accounting for insurance, maintenance, storage or berthing, fuel, repairs and taxes.

A longer term reduces the required monthly payment but increases total interest and may leave the loan balance higher than the boat’s resale value for a longer period. A shorter term increases monthly payments but normally reduces lifetime financing cost.

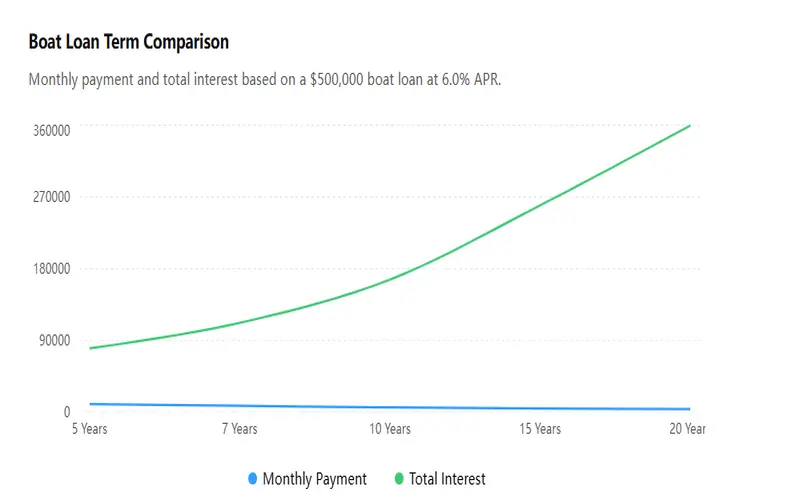

| Loan term | Estimated monthly payment | Total interest | Total repayment |

|---|---|---|---|

| 5 years | $2,027.64 | $21,658.37 | $121,658.37 |

| 10 years | $1,213.28 | $45,593.11 | $145,593.11 |

| 15 years | $955.65 | $72,017.38 | $172,017.38 |

| 20 years | $836.44 | $100,745.62 | $200,745.62 |

In this illustration, extending the term from 10 to 20 years lowers the monthly payment by about $377, but increases total interest by more than $55,000. The longest available term is therefore not automatically the most economical choice.

How to Reduce the Burden of Monthly Boat Loan Payments?

The burden of monthly boat loan payments is a top concern for many buyers, especially when it comes to luxury yachts or long-range cruising models. If monthly payments are too high, they can easily impact family or business cash flow. By carefully planning the loan term, down payment, and loan structure, you can effectively reduce the burden of monthly payments and make the cost of owning a yacht more manageable. Drawing on years of industry experience, I have summarized several practical methods:

Increase the Down Payment Ratio

The higher the down payment, the lower the principal balance, and consequently, the lower the monthly payments. Generally, For buyers with sufficient budgets, setting aside a substantial down payment in advance not only helps lower monthly payments but also qualifies them for more favorable interest rates when applying for a loan.

Extend the Loan Term

The longer the loan term, the lower the monthly repayment amount, but the total interest paid will increase accordingly. For buyers with limited cash flow or those who wish to maintain a comfortable lifestyle, choosing a 10–15-year or even 15–20-year loan can alleviate the pressure of monthly payments. Long-term loans are particularly suitable for vessels intended for investment, charter, or long-term cruising.

Choose a Loan Plan with a Lower Interest Rate

The interest rate directly affects your monthly payments. Before applying for a boat loan, it is advisable to compare rates from several banks or financial institutions and choose the fixed or variable rate plan that best suits your cash flow. Sometimes, increasing your down payment slightly can secure a lower interest rate, thereby reducing your monthly payments.

Utilize Loan Combinations Flexibly

Some financial institutions offer staged or combination loan plans, such as those with lower interest rates in the early years and gradual principal repayment later on. This approach can significantly reduce the burden of monthly payments in the early stages while ensuring reasonable long-term financial planning.

Manage Additional Fees and Insurance Costs

The pressure of monthly payments stems not only from principal and interest but also from insurance, mooring fees, and maintenance costs, which can increase your financial burden. When selecting a loan, factor the total cost of ownership over the entire loan term into your budget. This allows for a more accurate assessment of your monthly cash flow needs, helping you avoid excessive pressure from monthly payments.

What Conditions Can Improve the Approval Chances of a Boat Loan?

When reviewing a boat loan application, lenders not only consider the borrower’s credit profile but also carefully evaluate the vessel’s value, risk level, and future resale potential. A boat with clear ownership records, proper maintenance history, and stable market value is generally more likely to receive loan approval. The following factors can directly influence a lender’s approval decision.

Clear Ownership and Complete Title Records

When reviewing a boat loan application, lenders first verify the legal ownership of the vessel. A boat with complete registration records, clear ownership information, and no unresolved liens or ownership disputes allows lenders to better evaluate the collateral value and reduces potential risks during the approval process.

Provide a Recent Marine Survey Report or Valuation Document

The value of a boat can be affected by factors such as age, brand, equipment, condition, and market demand. Therefore, lenders usually require a professional marine survey report or valuation document to confirm the vessel’s actual market value. Recent evaluation documents can demonstrate that the boat is in good condition and that the requested loan amount is reasonable.

Maintain Verifiable Maintenance and Repair Records

Complete maintenance and repair records demonstrate how well the boat has been cared for over time and are an important factor when lenders assess its remaining value. Vessels with regular engine servicing, equipment inspections, and documented repairs generally carry lower risks and are more likely to receive approval from financial institutions.

The Boat’s Actual Condition Matches the Asking Price

Lenders will evaluate whether the boat’s purchase price accurately reflects its current market value. If the asking price is significantly higher than similar vessels on the market, the valuation may fall short, which could reduce the approved loan amount or affect the final approval decision. A reasonable price supported by accurate condition information can improve the chances of loan approval.

Provide Comparable Sales Data for Similar Boats

Recent transaction records for boats of the same brand, model, or similar specifications can help lenders evaluate market demand and resale potential. Vessels with strong demand in the used boat market and sufficient comparable sales data are generally easier for lenders to accept as collateral.

The Boat Can Obtain Required Insurance Coverage

Most lenders require the financed vessel to have valid insurance coverage to reduce risks related to accidents, damage, or total loss. A boat that qualifies for appropriate hull insurance and liability coverage demonstrates better risk management and can improve the likelihood of loan approval.

The Loan Amount Meets the Lender’s Minimum Financing Requirement

Different lenders may set minimum loan amounts based on their financing policies. If the requested loan amount is too small, it may not meet the lender’s evaluation and management requirements. Before applying, borrowers should confirm that the requested financing amount meets the lender’s minimum threshold.

The Boat’s Intended Use Complies with the Loan Agreement

Before choosing a boat, lenders typically review how the vessel will be used because private ownership, family cruising, and commercial operations involve different levels of risk. Buyers should also compare current new yachts for sale and used yachts for sale, considering factors such as model year, asking price, and overall condition. When the boat’s intended use matches the loan agreement—such as personal recreational use or properly authorized commercial operation—and the vessel has appropriate insurance coverage and qualifications, the loan application is more likely to receive approval.

Conclusion

When it comes to boat loans, a longer loan term isn’t necessarily the best choice, nor is a shorter term necessarily the most cost-effective. At its core, a boat loan is a financial planning decision that requires a comprehensive balance of three key factors: financial pressure, boat usage needs, and residual value. When actually purchasing a boat, factors such as the buyer’s cash flow, the boat’s average annual utilization rate, and future plans for boat replacement or upgrades will all influence the optimal choice of loan term. If opting for a short-term loan results in monthly payments that are too high and squeeze the budget allocated for insurance, berthing fees, maintenance, fuel, and emergency repairs, then a short-term loan is not an ideal solution.

Based on my long-term experience serving yacht clients, one point that many first-time buyers tend to overlook is focusing solely on whether they can afford the monthly payments, while neglecting the impact of the loan term on total interest costs and future asset flexibility. In fact, a reasonable loan structure is often more important than simply pursuing low monthly payments.

Taking into account market conditions and actual case studies, we can provide a relatively clear reference for categorizing boat loan terms:

- Weekend Recreational Boats: 5–10 years

Suitable for users primarily interested in family recreation and short-distance outings. Since these users typically don’t use their boats very frequently, a medium- to short-term loan is ideal for controlling total interest expenses and clearing the debt within a shorter timeframe, thereby leaving room for future upgrades.

- Long-Term Cruising Boats: 10–15 years

Suitable for users planning extended periods at sea or long-distance cruising. This loan structure strikes a balance between monthly payments and interest, reducing cash flow pressure while maintaining quality of life, and ensuring more stable and sustainable sailing plans.

- Investment/Charter Boats: 15–20 years

Suitable for users whose primary objective is commercial operation or rental income. A longer loan term significantly reduces monthly repayment pressure, making it easier for rental income to cover costs and thereby achieving a more stable cash flow structure.

Overall, the core principle in choosing a boat loan term is to ensure the loan structure serves your usage needs, rather than having your experience restricted by monthly payments. With proper planning, you can enhance capital efficiency while maintaining the long-term value and flexibility of your yacht asset. 👉Looking for a finance-friendly yacht? Explore our yacht listings and compare boat size, brand, age, price, and long-term ownership costs before making a purchase decision.

Disclaimer

This article is intended to provide reference information regarding boat financing and yacht loan terms. It is for educational and informational purposes only and does not constitute any form of loan, financial, tax, legal, or investment advice. The loan terms, interest rate ranges, monthly payment examples, and market data referenced in this article are based on publicly available information, industry research, and market experience as of 2026. Actual loan terms may vary depending on the borrower’s creditworthiness, down payment ratio, vessel age, vessel type, lender policies, and changes in market conditions.

The vessel types, brands, and financing cases mentioned in this article are provided solely as illustrative examples and do not constitute any promise of investment returns or guarantee of financing outcomes. Loan policies, interest rates, and relevant regulations are subject to change at any time; please refer to the latest information published by the lending institution. Neither the author nor this platform assumes any liability for any direct or indirect losses arising from the use of the information in this article.

About the Author

Andrew Rogers has long monitored developments in the yacht market, ship financing, and vessel transactions. Drawing on years of industry observation, he possesses in-depth research and understanding of the yacht purchasing process, loan planning, and vessel holding cost management. Andrew continuously monitors international yacht market trends, changes in ship loan policies, and the market performance of mainstream vessel models. Through objective data analysis and the compilation of industry case studies, he provides practical reference information for prospective buyers, helping them more comprehensively evaluate their yacht purchase budgets, financing options, and long-term ownership costs.

FAQ

Q1: How Long Can a Boat Loan Term Be?

A: For new boats from well-known brands, loan terms can extend up to 20 years, while used boats are typically financed for 12 years or less. Although longer loan terms increase the total interest paid over time, they can significantly reduce monthly payments. The ideal loan term should be based on your cash flow, budget, and intended use of the boat.

Q2: How Long Does Boat Loan Approval Take?

A: IThe approval period for ship‑financing loans usually depends on the lending institution, vessel assessment results and the completeness of application documents. Generally, it takes from several days to several weeks between application submission and final approval.

Q3: Can a Used Boat Qualify for a Long-Term Loan?

A: Used boats generally qualify for shorter loan terms than new boats. However, if the vessel is relatively new (typically 5 years old or less) and comes from a reputable brand, some lenders may offer financing terms of 10–12 years. Maintaining detailed service records, keeping the boat in good condition, and carrying valid insurance coverage can improve financing options.

Q4: Are There Penalties for Paying Off a Boat Loan Early?

A: Whether paying off the boat loan ahead of schedule incurs a penalty depends on the lender’s contract terms. Pre‑payment fees may be charged for some loans, and relevant rules should be carefully checked before application.

Q5: Is a Longer Boat Loan Term Always Better?

A: Not necessarily. A longer loan term lowers monthly payments and improves short-term cash flow, but it also increases the total interest paid over the life of the loan. Shorter-term loans require higher monthly payments but reduce overall financing costs. The best approach is to balance affordability, financial goals, and intended boat usage rather than focusing solely on achieving the lowest possible monthly payment.